Page 407 - Bank-Muamalat-AR2020

P. 407

405

Our Performance Sustainability Statement Governance Our Numbers Other Information

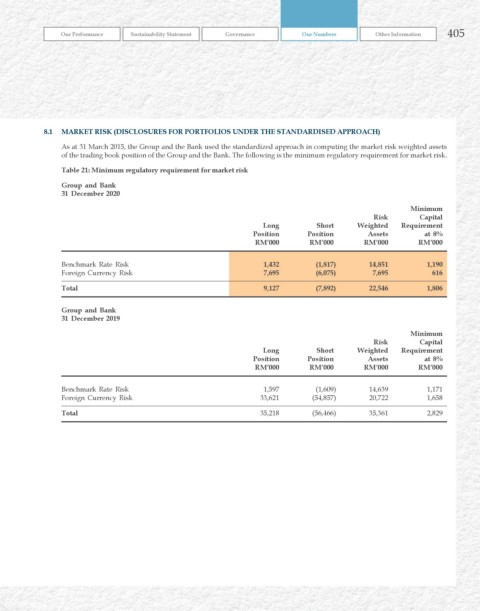

8.1 MArkET rISk (DISCLOSurES FOr POrTFOLIOS uNDEr ThE STANDArDISED APPrOACh)

As at 31 March 2015, the Group and the Bank used the standardized approach in computing the market risk weighted assets

of the trading book position of the Group and the Bank. The following is the minimum regulatory requirement for market risk.

Table 21: Minimum regulatory requirement for market risk

Group and Bank

31 December 2020

Minimum

risk Capital

Long Short weighted requirement

Position Position Assets at 8%

rM’000 rM’000 rM’000 rM’000

Benchmark Rate Risk 1,432 (1,817) 14,851 1,190

Foreign Currency Risk 7,695 (6,075) 7,695 616

Total 9,127 (7,892) 22,546 1,806

Group and Bank

31 December 2019

Minimum

risk Capital

Long Short weighted requirement

Position Position Assets at 8%

rM’000 rM’000 rM’000 rM’000

Benchmark Rate Risk 1,597 (1,609) 14,639 1,171

Foreign Currency Risk 33,621 (54,857) 20,722 1,658

Total 35,218 (56,466) 35,361 2,829