Page 411 - Bank-Muamalat-AR2020

P. 411

409

Our Performance Sustainability Statement Governance Our Numbers Other Information

8.4 LIquIDITy rISk

Liquidity and Funding risk

Liquidity risk is best described as the inability to fund any obligation on time as they fall due, whether due to increase in assets

or demand for funds from the depositors. The Bank will incur liquidity risk if it is unable to create liquidity and this has serious

implication on its reputation and continued existence.

In view of this, it is the Bank’s priority to manage and maintain a stable source of financial resources towards fulfilling the above

expectation. The Bank, through active balance sheet management, ensures that sufficient cash and liquid assets availability are

in place to meet the short and long term obligations as they fall due.

Generally, liquidity risk can be divided into two types, which are:

• Funding Liquidity Risk

Refers to the potential inability of the Bank to meet its funding requirements arising from cash flow mismatches at a

reasonable cost.

• Market Liquidity Risk

Refers to the Bank’s potential inability to liquidate positions quickly and insufficient volumes, at a reasonable price.

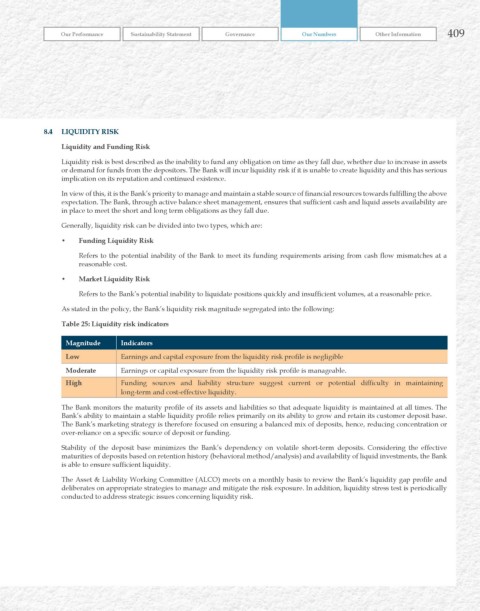

As stated in the policy, the Bank’s liquidity risk magnitude segregated into the following:

Table 25: Liquidity risk indicators

Magnitude Indicators

Low Earnings and capital exposure from the liquidity risk profile is negligible

Moderate Earnings or capital exposure from the liquidity risk profile is manageable.

high Funding sources and liability structure suggest current or potential difficulty in maintaining

long-term and cost-effective liquidity.

The Bank monitors the maturity profile of its assets and liabilities so that adequate liquidity is maintained at all times. The

Bank’s ability to maintain a stable liquidity profile relies primarily on its ability to grow and retain its customer deposit base.

The Bank’s marketing strategy is therefore focused on ensuring a balanced mix of deposits, hence, reducing concentration or

over-reliance on a specific source of deposit or funding.

Stability of the deposit base minimizes the Bank’s dependency on volatile short-term deposits. Considering the effective

maturities of deposits based on retention history (behavioral method/analysis) and availability of liquid investments, the Bank

is able to ensure sufficient liquidity.

The Asset & Liability Working Committee (ALCO) meets on a monthly basis to review the Bank’s liquidity gap profile and

deliberates on appropriate strategies to manage and mitigate the risk exposure. In addition, liquidity stress test is periodically

conducted to address strategic issues concerning liquidity risk.