Page 426 - Bank-Muamalat_Annual-Report-2023

P. 426

BANK MUAMALAT MALAYSIA BERHAD

BASEL II

PILLAR 3 DISCLOSURE

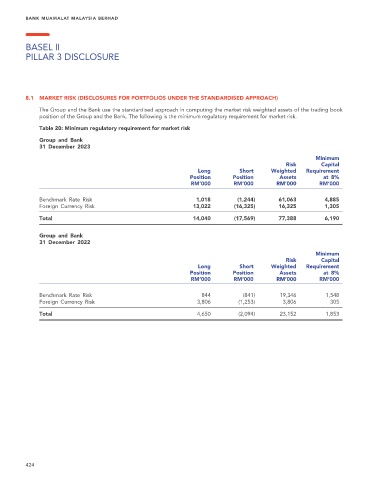

8.1 MARKET RISK (DISCLOSURES FOR PORTFOLIOS UNDER THE STANDARDISED APPROACH)

The Group and the Bank use the standardised approach in computing the market risk weighted assets of the trading book

position of the Group and the Bank. The following is the minimum regulatory requirement for market risk.

Table 20: Minimum regulatory requirement for market risk

Group and Bank

31 December 2023

Minimum

Risk Capital

Long Short Weighted Requirement

Position Position Assets at 8%

RM’000 RM’000 RM’000 RM’000

Benchmark Rate Risk 1,018 (1,244) 61,063 4,885

Foreign Currency Risk 13,022 (16,325) 16,325 1,305

Total 14,040 (17,569) 77,388 6,190

Group and Bank

31 December 2022

Minimum

Risk Capital

Long Short Weighted Requirement

Position Position Assets at 8%

RM’000 RM’000 RM’000 RM’000

Benchmark Rate Risk 844 (841) 19,346 1,548

Foreign Currency Risk 3,806 (1,253) 3,806 305

Total 4,650 (2,094) 23,152 1,853

424