Page 393 - Bank-Muamalat-Annual-Report-2021

P. 393

ANNUAL REPORT 2021 391

SUSTAINABILITY STATEMENT OUR GOVERNANCE OUR NUMBERS OTHER INFORMATION

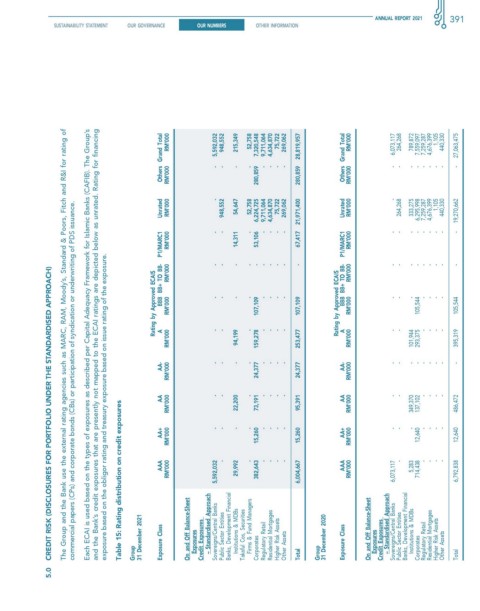

Each ECAI is used based on the types of exposures as described per Capital Adequacy Framework for Islamic Banks (CAFIB). The Group’s

and the Bank’s credit exposures that are presently not mapped to the ECAI ratings are depicted below as unrated. Rating for financing

The Group and the Bank use the external rating agencies such as MARC, RAM, Moody’s, Standard & Poors, Fitch and R&I for rating of

others grand Total rM’000 rM’000 5,592,032 - 948,552 - 215,349 - 52,758 - 7,320,548 280,859 9,711,064 - 4,634,870 - 75,722 - 269,062 - 280,859 28,819,957 others grand Total rM’000 rM’000 6,073,117 - 264,268 - 789,872 - 7,559,097 - 7,259,287 - 4,676,399 - 1,105 - 440,330 - 27,063,475 -

unrated rM’000 - 948,552 54,647 52,758 6,224,725 9,711,064 4,634,870 75,722 269,062 67,417 21,971,400 unrated rM’000 - 264,268 333,275 6,295,998 7,259,287 4,676,399 1,105 440,330 19,270,662

commercial papers (CPs) and corporate bonds (CBs) or participation of syndication or underwriting of PDS issuance.

P1/MArc1 rM’000 rM’000 - - - - 14,311 - - - 53,106 - - - - - - - - - - P1/MArc1 rM’000 rM’000 - - - - - - - - - - - - - - - - - -

exposure based on the obligor rating and treasury exposure based on issue rating of the exposure.

creDIT rIsK (DIsclosures for PorTfolIo unDer The sTAnDArDIseD APProAch)

rating by Approved ecAIs BB+ To BB- BBB rM’000 - - - - 107,109 - - - - 107,109 rating by Approved ecAIs BB+ To BB- BBB rM’000 - - - 105,544 - - - - 105,544

rM’000 A - - 94,199 - 159,278 - - - - 253,477 A rM’000 - - 101,944 293,375 - - - - 395,319

AA- - - - - - - - - 24,377 AA- - - - - - - - - -

rM’000 24,377 rM’000

AA - - - - - - - AA - - - - - -

rM’000 22,200 73,191 95,391 rM’000 349,370 137,102 486,472

Table 15: rating distribution on credit exposures

AA+ rM’000 - - - - 15,260 - - - - 15,260 AA+ rM’000 - - - 12,640 - - - - 12,640

AAA rM’000 5,592,032 - 29,992 - 382,643 - - - - 6,004,667 AAA rM’000 6,073,117 - 5,283 714,438 - - - - 6,792,838

31 December 2021 exposure class on and off Balance-sheet exposures credit exposures – standardised Approach Sovereigns/Central Banks Public Sector Entities Banks, Development Financial Institutions & MDBs Takaful Cos, Securities Firms & Fund Managers Regulatory Retail Residential Mortgages Higher Risk Assets Other Assets 31 December 2020 exposure class on and off Balance-sheet exposures credit exposures – standardised

group Corporates Total group Corporates Total

5.0