Page 296 - Bank-Muamalat-AR2020

P. 296

294 BANK MUAMALAT MALAYSIA BERHAD About Us Our Leadership Our Strategy

ANNUAL REPORT FY2020

Notes to the fiNaNcial statemeNts

31 December 2020 (16 JamaDil awal 1442h)

46. FINANCIAL rISk MANAGEMENT OBJECTIvES AND POLICIES (CONT’D.)

(a) Credit risk (cont’d.)

(ii) Credit quality for financing of customers (cont’d.)

Past due but not impaired (cont’d.)

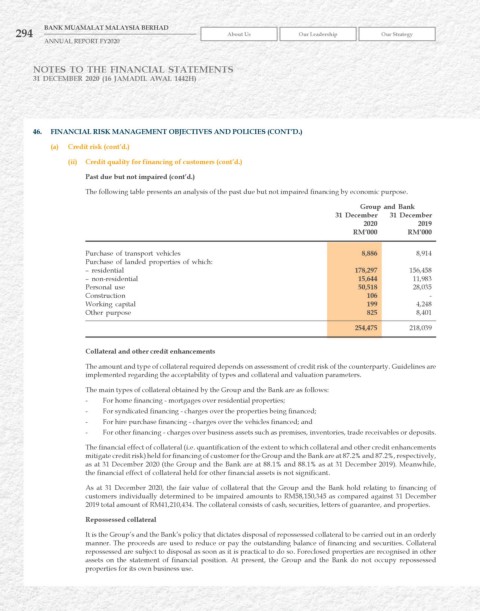

The following table presents an analysis of the past due but not impaired financing by economic purpose.

Group and Bank

31 December 31 December

2020 2019

rM’000 rM’000

Purchase of transport vehicles 8,886 8,914

Purchase of landed properties of which:

– residential 178,297 156,458

– non-residential 15,644 11,983

Personal use 50,518 28,035

Construction 106 -

Working capital 199 4,248

Other purpose 825 8,401

254,475 218,039

Collateral and other credit enhancements

The amount and type of collateral required depends on assessment of credit risk of the counterparty. Guidelines are

implemented regarding the acceptability of types and collateral and valuation parameters.

The main types of collateral obtained by the Group and the Bank are as follows:

- For home financing - mortgages over residential properties;

- For syndicated financing - charges over the properties being financed;

- For hire purchase financing - charges over the vehicles financed; and

- For other financing - charges over business assets such as premises, inventories, trade receivables or deposits.

The financial effect of collateral (i.e. quantification of the extent to which collateral and other credit enhancements

mitigate credit risk) held for financing of customer for the Group and the Bank are at 87.2% and 87.2%, respectively,

as at 31 December 2020 (the Group and the Bank are at 88.1% and 88.1% as at 31 December 2019). Meanwhile,

the financial effect of collateral held for other financial assets is not significant.

As at 31 December 2020, the fair value of collateral that the Group and the Bank hold relating to financing of

customers individually determined to be impaired amounts to RM58,150,345 as compared against 31 December

2019 total amount of RM41,210,434. The collateral consists of cash, securities, letters of guarantee, and properties.

repossessed collateral

It is the Group’s and the Bank’s policy that dictates disposal of repossessed collateral to be carried out in an orderly

manner. The proceeds are used to reduce or pay the outstanding balance of financing and securities. Collateral

repossessed are subject to disposal as soon as it is practical to do so. Foreclosed properties are recognised in other

assets on the statement of financial position. At present, the Group and the Bank do not occupy repossessed

properties for its own business use.