Page 319 - Bank-Muamalat-AR2020

P. 319

317

Our Performance Sustainability Statement Governance Our Numbers Other Information

46. FINANCIAL rISk MANAGEMENT OBJECTIvES AND POLICIES (CONT’D.)

Total rM’000 18,955,006 6,303 8,444 77,546 52,316 43,823 9,272 459,633 - 250,532 502,517 20,365,392 2,462,291 (21,859) 77,546 2,517,978 (b) Market risk (cont’d.)

Types of market risk (cont’d.)

-

-

-

-

-

-

-

-

-

-

-

Others rM’000 4,677 30 4,707 (1,329) (1,329) (ii) Non-traded market risk (cont’d.)

Foreign exchange risk (cont’d.)

-

-

-

-

-

-

-

-

-

-

-

-

-

-

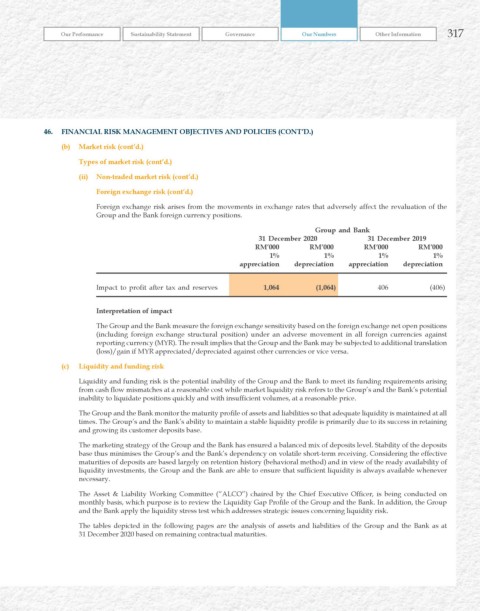

Canadian Dollar rM’000 3,332 3,332 Foreign exchange risk arises from the movements in exchange rates that adversely affect the revaluation of the

Group and the Bank foreign currency positions.

Group and Bank

Japanese yen rM’000 - - - - - - - - - - - - 21,305 - - 21,305 rM’000 rM’000 rM’000 rM’000

31 December 2019

31 December 2020

1% 1% 1% 1%

Great Britain Pound rM’000 2,257 - - - (73) - - - - - - 2,184 1,218 - - 1,218 appreciation depreciation appreciation depreciation

Impact to profit after tax and reserves 1,064 (1,064) 406 (406)

Euro rM’000 3,980 4,047 868 868 Interpretation of impact

- - - 67 - - - - - - - -

FINANCIAL rISk MANAGEMENT OBJECTIvES AND POLICIES (CONT’D.)

The Group and the Bank measure the foreign exchange sensitivity based on the foreign exchange net open positions

Swiss Franc rM’000 280 280 (including foreign exchange structural position) under an adverse movement in all foreign currencies against

- - - - - - - - - - - - - -

reporting currency (MYR). The result implies that the Group and the Bank may be subjected to additional translation

(loss)/gain if MYR appreciated/depreciated against other currencies or vice versa.

2,021 - - - - - - - - - - 2,021 - - (c) Liquidity and funding risk

Australian Dollar rM’000 (177) (177) Liquidity and funding risk is the potential inability of the Group and the Bank to meet its funding requirements arising

from cash flow mismatches at a reasonable cost while market liquidity risk refers to the Group’s and the Bank’s potential

united States Dollar rM’000 397,166 - 1 - 200 69 20 - - - - 397,456 (66,128) - - (66,128) inability to liquidate positions quickly and with insufficient volumes, at a reasonable price.

The Group and the Bank monitor the maturity profile of assets and liabilities so that adequate liquidity is maintained at all

times. The Group’s and the Bank’s ability to maintain a stable liquidity profile is primarily due to its success in retaining

52,122

6,303

19,954,977

502,517

43,754

18,544,905

9,252

250,532

-

459,633

77,546

2,558,609

2,502,922

8,413

77,546

Malaysian

rM’000

ringgit

and growing its customer deposits base.

(21,859)

The marketing strategy of the Group and the Bank has ensured a balanced mix of deposits level. Stability of the deposits

base thus minimises the Group’s and the Bank’s dependency on volatile short-term receiving. Considering the effective

maturities of deposits are based largely on retention history (behavioral method) and in view of the ready availability of

necessary.

Market risk (cont’d.) Types of market risk (cont’d.) Non-traded market risk (cont’d.) Foreign exchange risk (cont’d.) Bank 31 December 2019 Liabilities Deposits from customers Deposits and placements of banks and other financial institutions Bills and acceptances payable Islamic derivative financial liabilities Other liabilities Lease liabilities Provision for taxation and zakat Recourse obligation on financing sold to Cagamas Deferred tax liab

The Asset & Liability Working Committee (“ALCO”) chaired by the Chief Executive Officer, is being conducted on

monthly basis, which purpose is to review the Liquidity Gap Profile of the Group and the Bank. In addition, the Group

and the Bank apply the liquidity stress test which addresses strategic issues concerning liquidity risk.

The tables depicted in the following pages are the analysis of assets and liabilities of the Group and the Bank as at

(b) (ii) 31 December 2020 based on remaining contractual maturities.

46.